Applied Optoelectronics, Graded

The cleanest pure-play supply-control story on the board, paired with some of its weakest owner economics.

Note to readers: This is part of the "Time to Grade the Connectivity Layer" series.

Applied Optoelectronics is the strangest name on the connectivity board. It may control one of the tightest supply points in AI optics. It also carries some of the weakest economics on the board.

I have written about it once already, after the Q1 print, and the conclusion then was that the company confirms the AI optics bottleneck without yet proving the economics of it. This card runs that instinct through the framework, the same five tests every name on the board has to clear, with the conclusion withheld until the marks are in.

What makes AOI different from the rest of this layer is that it is a manufacturer rather than a fabless designer, and underneath two businesses that look unrelated sits a single asset the rest of the industry is currently short of. Most investors meet it as an 800G transceiver story, but it is a laser company first. It started almost thirty years ago out of a semiconductor laser research group at the University of Houston, and the indium phosphide fab it runs today has existed since 2000. That means it has made the hardest part of an optical transceiver in-house for twenty-six years, which matters because the scarce input across the optics chain in 2026 is the laser itself, the part most transceiver makers have to buy.

On top of the fab sit two revenue lines. The datacenter business, $81.4 million in Q1 and up 154% year over year, builds optical transceivers across 100G, 400G, 800G and now 1.6T, and it crossed over to become larger than the cable business this quarter for the first time in a while. The CATV business, $66.8 million, sells smart amplifiers into operators like Charter, with a microprocessor control algorithm and an AI-driven telemetry software layer, QuantumLink, riding on top. In May the company was named primary vendor for Mediacom’s DOCSIS 4.0 upgrade across roughly a million homes, which makes the cable line a live upgrade cycle with named wins, the quieter revenue base that helps fund part of the ramp beside it. On the board AOI sits in the optical transceiver layer, and the question this card has to settle is whether the company controls anything in that layer or merely ships into it.

The manufacturing model is the last piece to understand before the marks make sense. AOI builds its own production equipment in-house and has spent more than a decade automating the transceiver line, which is why management can talk about copying a line from Taiwan into Texas as a paste operation rather than a redesign. That automation is what makes a US manufacturing footprint economically possible at all, and it is the reason equipment lead times have not yet bitten them the way they have bitten peers buying the same tools on the open market.

So the setup is a company with a genuinely scarce asset, a credible plan to scale it, demand it says runs ahead of supply through mid-2027, and a set of financials that do not yet look like any of that has reached the owner. Q1 revenue grew 51% year over year to a record $151.1 million, non-GAAP gross margin fell to 29.2% from 31.4% the quarter before, and the company is still losing money. I already take the demand as real. What the card has to settle is whether the evidence in the filings earns AOI the tier I am about to give it.

What the margin is doing while the revenue climbs

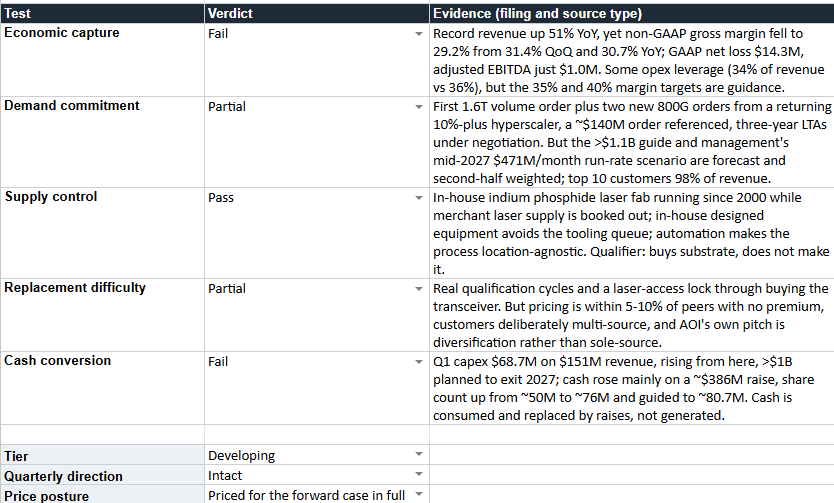

Economic capture asks whether growth turns into stronger economics rather than just more revenue, and for AOI the honest answer is no, not yet. Revenue grew 51% year over year and 13% sequentially to a record, and over the same stretch non-GAAP gross margin went the wrong way, 30.7% a year ago, 31.4% last quarter, 29.2% now. GAAP net loss was $14.3 million, non-GAAP net loss was $4.9 million, and adjusted EBITDA was positive by all of $1.0 million. The company is selling more and keeping less of each dollar as it does.

One thing does cut the other way, since the test is about more than gross margin alone. Operating expenses fell to 34% of revenue from 36% a year ago, so some operating leverage is forming as the top line scales. But the central line of the test, whether the company keeps more of what it sells as it grows, is not being met today. Management is explicit that the near-term mix is a headwind and points to roughly 35% gross margin by the end of this year and 40% by the end of next, and both remain targets the numbers have not reached. Economic capture is the clearest mark on the card to call, a Fail, because the proof the test demands still sits in the guidance instead of the results.

How much of the ramp is actually ordered

Demand commitment asks how much of future demand is underwritten by something binding, backlog, prepayments, purchase commitments or repeated production orders, rather than by management confidence. AOI scores better here than the income statement suggests, though the quality of the demand evidence is still very different from the cleaner connectivity names on the board. During the quarter it took its first volume order for a 1.6T transceiver from a long-standing major hyperscale customer, along with two new 800G volume orders from that same customer, and it expects that account to return as a 10%-plus customer. Thompson Lin referenced a single order in the region of $140 million and described three-year long-term agreements under negotiation with several customers, covering lasers and the ELSFP modules as well as transceivers.

That is real, named, repeated-order evidence, more binding than management guidance even if orders can still be cut, delayed or rephased, which AOI’s own risk language is careful to flag. The part that holds the mark back is everything stacked on top of it. The raised full-year guide of more than $1.1 billion, the internal $1.2 billion target, the $1.4 billion to $1.5 billion of demand management says actually exists, the roughly $471 million per month of datacenter transceiver revenue management sketches for mid-2027 as its own run-rate scenario, up from $378 million at the prior call, all of that is forecast and second-half weighted, and the long-term agreements are still in negotiation rather than signed. Concentration sharpens the point. The top ten customers were 98% of revenue, with three names above 10%. Binding orders exist and recur, but the case the equity now rests on is mostly forecast, so the mark is Partial.

The laser inside the bottleneck

Supply control is the test that catches a company riding a hot theme while the scarce thing sits in someone else’s hands, and it is where AOI separates itself from the broader field of transceiver makers. The scarce thing in optics right now is the indium phosphide laser, and AOI makes its own. Management was blunt about what that means competitively. Lasers from the merchant suppliers, Lumentum, Coherent, even Broadcom and Sumitomo, are effectively booked out, and as Lin put it, without a laser you cannot build a transceiver. A company that owns its laser fab in a market where lasers are the binding constraint controls something its rivals are currently queuing for. The scale behind that is concrete. AOI exited Q1 at roughly 100,000 transceivers a month and guides to over 930,000 a month of 800G and 1.6T by the end of 2027, more than half of it from Texas, while expanding laser fabrication capacity by about 350% over the same window. Since each of the harder 800G and 1.6T modules carries four or more lasers, that unit ramp is really a laser ramp, which is the precise reason owning the fab is the part that matters.

The control runs deeper than the fab. AOI designs its own production equipment, which means it is largely not competing for the same machinery that everyone else is bidding up, and equipment availability has not been a constraint for it to date. The automation that follows from that makes its process location-agnostic, which is what turns a US footprint from an aspiration into a copy-paste of an existing Taiwan line. I cross-checked the laser-shortage claim against Fabrinet, Lumentum and Coherent when I wrote about the quarter, and they describe the same constraint from their own seats, which is why I treat it as structural and not a claim made in self-interest.

The honest qualifier is one layer up. AOI does not make the indium phosphide substrate, it buys it, from four or five suppliers with most outside China, and it holds roughly a year of inventory. The substrate situation is bound up in US-China politics more than in any true global capacity shortage, which cuts both ways, a political problem can ease as fast as it appeared. The company controls the laser fab, which is the link the rest of the chain has to pass through, even if it does not control the raw wafer feeding it. On balance that is a Pass, and it is the mark that lifts AOI above a pure capacity story.

There is a larger version of this still to come, and it belongs in the optionality column instead of in the mark. As the industry moves toward co-packaged optics, the laser leaves the transceiver and becomes an external light source, the ELSFP module, built around the 300 to 400 milliwatt high-power lasers AOI already makes in-house and plans to ramp toward roughly 400,000 pieces a month by the end of 2027. In that world AOI moves from transceiver supplier to supplying the light source for the rack itself, which is where the three-year agreements still under negotiation point. None of that is in the numbers yet, so it does not lift the Pass any higher than the laser fab already does. Its value is that the moat could widen as the architecture changes, at a point where most of the field would have to start the laser problem from scratch.

Whether the customer is actually stuck

Replacement difficulty asks what gets harder, slower or more expensive for a customer who switches away, and here the evidence is mixed in a way that matters for the tier. The friction is real. Qualifying a new transceiver vendor takes time, and AOI completed 800G qualification with a second hyperscaler this quarter after starting volume shipments to the first, which makes the qualification cycle a genuine cost to anyone trying to switch. The laser synergy adds a genuine lock, because the only way to access AOI’s fab capacity is to buy its transceivers, which is exactly the security a supply-anxious hyperscaler is looking for.

But the same management that describes that lock also describes the limits of it. Pricing sits within 5% to 10% of competitors, with no real premium, and AOI blends its US and Asian cost so the customer does not see a step-up. Customers are deliberately pursuing multi-vendor strategies, and AOI’s own pitch is supply-chain diversification, which by definition means being one qualified source among several rather than the only one. Lin noted that easier products, multi-mode and DR4, can be sourced from the likes of Fabrinet, and the differentiation concentrates at 800G and 1.6T where the four-laser modules make the in-house fab decisive. The switching cost exists and is rising with the laser dependence, but the customer is choosing AOI partly because it does not want to be stuck with anyone, so the mark is Partial.

What the ramp costs before it pays

Cash conversion asks whether growth is turning into cash per share or whether capex, working capital and dilution are absorbing the economics before they reach the owner, and this test earned its place on exactly this kind of company. AOI spent $68.7 million on capex in Q1 against $151 million of revenue, expects quarterly capex above that level for the rest of the year, and frames a total investment north of $1 billion to reach roughly a million transceivers a month exiting 2027. The funding mix is stated plainly, cash on hand, cash from operations, equity sales and additional debt.

The dilution is already in the numbers. Cash rose to $449.4 million from $216 million, but that jump is largely financing, with additional paid-in capital up nearly $386 million and the weighted basic share count up from about 50 million a year ago to 76 million, guided to roughly 80.7 million next quarter. This is a manufacturing ramp funded by the capital markets while the business runs a loss. Management’s counter is that each capacity increment pays back in eight or nine months once it runs at target margin, which is a strong return if the margin arrives. Today it has not, the cash is being consumed and replaced by raises rather than thrown off, and the owner’s slice is being diluted on the way through, so the mark is Fail.

Since the Q1 print the filings have made that capital intensity more concrete. On May 8 the company signed three 123-month Houston leases covering more than 736,000 square feet, each carrying an option to buy the building and land for an aggregate $102.25 million, on top of a separate Pearland property purchase of around 388,000 square feet for roughly $58 million. In early June shareholders approved a new equity incentive plan, so share issuance stays part of the structure that funds all of this. None of it breaks the thesis. What it does is make the owner-economics question harder to set aside, because the company is physically rebuilding its manufacturing footprint to chase the opportunity, and the bill for that build is landing well before the margin proof does.

The bear case the tier has to survive

The tier has to survive the argument I would make against AOI myself, which is that this is a capital-intensive, low-margin manufacturer dressed in a bottleneck narrative, and that the laser advantage is real but the equity captures too little of it. There is weight to that. A 29% gross margin on a loss-making base, capex above 40% of revenue, and a rising share count is the financial signature of a business where the value leaks out before it reaches the owner, however good the end market.

The bear is right on today’s numbers, which is why the rebuttal does not try to argue with them. It rests instead on the supply-control evidence being proven and already shipping, a different starting point from a transceiver assembler buying lasers on the open market and hoping margins scale. That difference is the entire reason this name does not sit one tier lower. Whether it earns a tier higher depends on the two marks that failed, and those are a matter of execution that has not happened yet.

What the price has already decided

Price keeps its own column, because what a business is worth and what you pay for it are different facts, and AOI is a sharp illustration of why. The stock has traded as a momentum optics name, up several hundred percent over the past year, and the posture I read is the most demanding the board uses. At roughly $13.5 billion of market value and around $170 a share against trailing losses in mid-June, the price already discounts the 2027 ramp arriving close to management’s own version of it. The price assumes the capacity ramp converts to the guided revenue and that gross margin climbs toward the mid-thirties this year and toward forty next.

The detail worth holding onto is what that price is actually paying for. The revenue ramp and the margin expansion it assumes in full are precisely the two marks this card could not clear, demand commitment at Partial and economic capture at Fail. The price is not really rewarding the part AOI has already proven. It is rewarding the part AOI still has to prove. I am not putting a precise figure on the valuation here without a fresh primary-source read, but the posture is clear enough without one.

The card

Tier: Developing. AOI holds a clear position on the critical path with a supply-control advantage that is proven and shipping today rather than promised, which keeps it above a pure capacity story. But economic capture and cash conversion are not yet there, which keeps it below Confirmed. Developing is exactly the seat for a real moat element wrapped in unproven economics.

Quarterly direction: Intact. The demand and supply-control legs firmed up, first 800G shipments, a first 1.6T order, a raised full-year guide and capacity tracking slightly ahead. The economic-capture leg weakened, with margin compressing as the ramp began. They net to Intact, because the one mark that would change the tier, margin, did not move in the direction that would change it.

Price: Priced for the forward case to be delivered in full. The multiple is paying for the revenue ramp and the margin expansion, which are the two marks the card could not clear.

When this is a position worth taking

A tier is not a recommendation, and Developing in particular describes a business you would be underwriting on execution instead of on proven results. That makes it a question of temperament as much as of price. An investor who wants the economics already visible in the numbers has a clean reason to wait, since the print that would move this to Confirmed is also the one that takes most of the guesswork out, and the rules below say what that print has to contain. For that investor the honest answer is the watchlist, which is where I keep it.

The case suits a different appetite. If you are comfortable owning the laser bottleneck specifically, can sit through capex-heavy cash burn and equity issuance while the second-half ramp either proves the economics or does not, and you size the position knowing the whole tier rests on a single Pass, then AOI is a coherent way to express that view before the proof lands, accepting that you are paying for a forecast the market has only partly taken the risk out of. The grade does not try to talk anyone in or out of that. Its only job is to be precise about what you would be buying, a genuine supply-control position wrapped in economics that have not yet arrived.

What I am holding the placement against

Developing is a claim I have to be able to defend, and for AOI the defense is narrow and specific. The tier rests on supply control, the in-house laser fab in a laser-short market, and nothing else is doing the load-bearing work. Two Fails, two Partials and a single Pass would normally argue for a lower tier, and the reason it does not here is that the one Pass falls on the test that matters most for this particular name. Everything that would move the placement from here is mechanical, and worth stating as rules rather than hopes.

Moves to Confirmed if: non-GAAP gross margin clears the low-to-mid thirties, the 800G ramp inflects on the volume and revenue trajectory management laid out, the long-term agreements move from negotiation to signed, and the capacity build leans less on equity funding. That is the combination that turns economic capture and cash conversion from Fail into evidence, and it is also the print that would settle the question that has kept the name off the basket.

Stays Developing if: revenue ramps as guided but gross margin stays stuck near 29%. At that point the laser advantage is real and the owner still is not capturing it, so the tier does not advance no matter how large the revenue gets.

Moves lower if: the supply-control evidence itself weakens. If merchant laser supply loosens, if AOI’s own fab ramp slips, or if dilution accelerates ahead of any margin proof, the single mark holding the placement up gives way and Developing is no longer defensible.

The next real datapoint is the Q2 call on August 6. Until then the placement holds, resting entirely on the one thing the company genuinely controls.

Disclosure: The Best Ideas 2026 basket is ten equal weighted positions: Nvidia, Broadcom, Cadence, Vertiv, Powell Industries, Eaton, Hubbell, Arista, Credo and Astera Labs. The basket does not hold Applied Optoelectronics; it remains on the watchlist pending margin proof. Family account positions are disclosed separately when relevant. Applied Optoelectronics is not part of any family portfolio as per today either. This is my own research and personal opinion, not investment advice. Do your own work before acting on anything here.