Astera Labs, Graded

Easy to admire, hard to add to at this price.

Key takeaways

Q1 revenue was $308.4 million, up 14% sequentially and 93% year over year, at a 76.4% non-GAAP gross margin and a 36.2% non-GAAP operating margin. On the test that asks whether a company keeps more of what it sells as it scales, this is the cleanest card the board has graded.

Content per accelerator has gone from the $50 to $100 range at IPO to more than $1,000 today, with a 20% to 25% ASP step each retimer generation. The capture is structural, the product of many quarters.

The moat that earns the placement is already in place. COSMOS is wired into how hyperscalers run their fleets and carries across the product line at little extra cost, and few AI systems ship without an Aries part inside. The switching cost is already sunk on the customer’s side.

The test that stays open is supply control. Astera is fabless, sits on the bottleneck without owning the capacity, and the CFO acknowledged the same supply tightness the rest of the chain is living with.

The exciting half of the story, Scorpio scale-up fabric, optical, UALink and custom, is design wins and 2027 revenue rather than shipped product. How that splits across the five tests, and where it leaves the name, is below.

Astera is easy to like, and it has been good to me. The hard part is working out which Astera the stock is actually pricing. The one already shipping into AI systems, or the one management is still building toward 2027 and 2028.

It is really two companies wearing one ticker. Underneath sits the signal conditioning franchise and the software that runs it. Proven, repeatable, already paying. On top sits the rack-architecture ambition, the scale-up fabric, the optical engine, UALink, the custom silicon, almost all of it still years out. The market prices the two as one number. Pulling that number apart is the whole job here.

It is also why Astera is the hardest name I have graded so far. It already sits in my Best Ideas 2026 basket, and it is up around 100% this year. A position that has been that good to you is exactly the one you are tempted to wave through. So the marks below stay tied to the filings, and I have saved the hardest look for the test where Astera is weakest rather than the one where it shines.

I wrote about Astera once already this cycle, after the Q1 print and the J.P. Morgan fireside. The read then was that a very clean quarter was hiding a transition, the company turning from a connectivity supplier into a piece of how the AI rack itself gets built. I flagged where that ambition gets tested. Customer concentration, CXL timing, the Scorpio ramp. And I noted that the valuation already assumes most of it lands on time. This card runs the same instinct through the framework, the five tests every name in my connectivity dive has to clear, with the verdict held back until the marks are in.

What ships today, and what is still a slide

Here is that split in detail, because the grade turns on which side of it each piece of evidence lands.

What ships today is the signal conditioning portfolio and COSMOS, the software layer that started life as the retimer differentiator. PCIe Gen 6 is already over a third of revenue and shipping in real volume, and on the Evercore stage Astera put Aries in almost every AI system in the field. COSMOS sits a layer down inside how customers run their estates, and the same framework carries across Aries, Taurus, Leo and Scorpio. This is the half that is real in the numbers.

The other half is still a slide, and it is most of what the bulls are paying for. Scorpio X, the scale-up fabric switch, is shipping early volumes, with the flagship 320-lane part due to ramp to volume production in the second half of this year. UALink switches line up behind an Amazon and AMD launch in 2027, with revenue closer to 2028. The optical roadmap lands in stages across 2027 and 2028. The custom wins, NVLink Fusion and the memory work among them, are 2027 revenue. The NVLink Fusion one is worth a pause, because a design win inside a Nvidia-led architecture does not lock in the economics. Sitting in that stack is bullish. But Nvidia holds most of the leverage over economics, timing and partner hierarchy, so being there on its own tells you little about durable pricing power. The engagement is real. It just has not turned into shipped and billed product yet, and keeping that line straight is the whole job of this card.

What the margin does as the revenue compounds

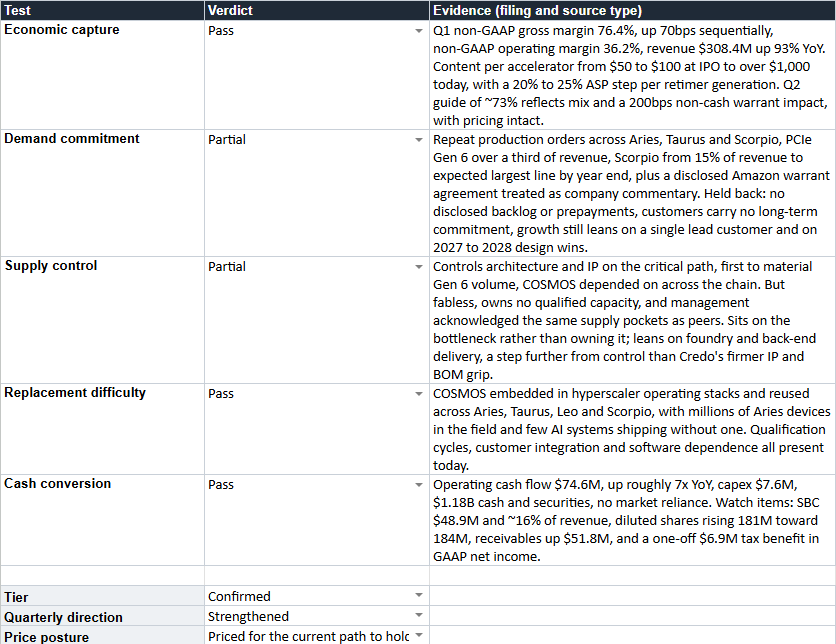

Economic capture is the test for whether scale actually pays. Does the company keep more of each dollar as it grows, or just print more revenue?

Astera answers it better than anything I have graded so far. Non-GAAP gross margin was 76.4% in Q1, up 70 basis points on the quarter, and the non-GAAP operating margin was 36.2% on revenue that grew 93% year over year.

The deeper proof is the content trajectory. A company that sold $50 to $100 of content per accelerator at the IPO now sells more than $1,000, and management points to a 20% to 25% step in ASP with each generation, because every new generation carries more speed and capability the customer pays up for. That is the test passing in the numbers, more kept per dollar as the thing scales.

The one qualifier is the Q2 gross margin guide of roughly 73%, down from 76%. That step is mix and a 200 basis point non-cash hit from a customer warrant, with underlying pricing intact, and the same management expects margin to climb back as the mix normalizes.

So the mark is a clear Pass.

How much of the ramp is actually ordered

Demand commitment is about how much of the future is actually underwritten, by backlog, prepayments, purchase commitments or repeat production orders, instead of by management telling you it is coming.

Astera scores well here, though not all the way to a Pass. The credit is real and broad. Repeat production orders run across Aries, Taurus and Scorpio, PCIe Gen 6 is already a third of the company, and Scorpio has gone from 15% of revenue last year to a line management expects to be its largest by year end.

Astera has also disclosed a warrant agreement with Amazon, which reads as a deeper customer tie. I am treating it as company-disclosed commentary rather than a verified commitment, because the binding terms sit in filings I have not gone through for this card.

What holds the mark back is everything the valuation leans on. Astera itself lists the absence of long-term customer commitments as a risk factor. There is no disclosed backlog or prepayment to put a number on. And a large share of the forward case rests on design wins out in 2027 and 2028. The demand that is committed is the demand already shipping. The demand the price needs is still being described.

Concentration earns its own hard look. In a company whose numbers otherwise look close to perfect, it is the single biggest risk. Management is open that a lot of the growth still runs through one lead customer, with the diversification, two more hyperscalers on Scorpio P, set as a second-half event rather than a present one. A customer that size shapes far more than order volume. It can lean on timing, product mix, working capital, roadmap priorities and the margin story, and the warrant that clips the Q2 gross margin guide is a small, visible piece of that. The accounting hit is non-cash, but the warrant itself is a reminder that a buyer this big bargains over the economics of a deal.

That is the same line I drew in May, when I flagged concentration and CXL timing as the places this story gets tested, and it is why the mark here is Partial rather than Pass.

Whose hands the bottleneck sits in

Supply control is the test that catches a company riding a hot theme while the scarce thing sits in someone else’s hands. It is also the mark where it would be easiest to flatter a name I own, so it gets the hardest look.

Astera controls architecture and IP on the critical path. It was first to material Gen 6 volume when nobody else was, and COSMOS is a software position the rest of the chain has come to lean on. You cannot build a dense AI rack without this layer of connectivity silicon, so in that sense Astera sits on the bottleneck.

It does not own it, though. Astera is fabless. It designs the silicon and the software, but the qualified capacity belongs to its foundry and back-end partners, and the CFO was clear that Astera runs into the same pockets of supply tightness as everyone else, handled through a diversified back end with supply locked through year end.

So on my read, Astera sits on the constraint without owning it. The contrast with Credo earlier in this series is a difference of degree rather than a clean divide. Both are fabless, both depend on partners to build what they design, and neither owns the constraint outright. Credo’s edge is a firmer grip on its own IP and the bill of materials around it, the core silicon and the optical content, which buys it more say over what gets made and on what terms. Astera leans harder on a foundry and a back end actually delivering when it is needed, which puts it a step further from control. The mark is Partial, and that Partial is one of the things the Confirmed tier has to survive.

Why the customer does not leave

Replacement difficulty asks a simple question. What breaks, slows down or gets more expensive for a customer who tries to switch away?

This is where Astera’s moat actually lives. COSMOS is wired in at a fundamental layer of hyperscaler operations, built up over years of signal conditioning work and now reused with the fabric portfolio at low cost to the customer and high cost to anyone trying to displace it.

In plain terms, COSMOS is the software a hyperscaler runs its fleet through, which makes Astera part of how the customer operates rather than a chip it buys once. Once that is wired into how the estate runs, the cost of ripping it out is the moat. Add the installed base, a very large fleet of Aries parts already in the field and the know-how that comes with them, and the three things the test looks for are all here. The time and cost to qualify a rival. The customer-specific integration. The dependence on Astera’s own software.

None of this means Astera has the field to itself. On retimers, CXL and the rest of the signal-conditioning layer it lines up against Broadcom, Marvell, Montage and a field of connectivity-IP vendors, with the ever-present option for a hyperscaler to take the work in-house.

On scale-up fabric the fight is as much about architecture as about vendor, with Nvidia’s NVLink and NVSwitch, Ethernet pushed into scale-up, UALink and proprietary hyperscaler designs all chasing the same place in the rack. So the split runs like this. Replacement difficulty is high and proven on the incumbent base that ships today, where COSMOS and the Aries fleet do the work, and wide open on the fabric layer the price is most excited about, where Astera is early and well placed but a long way from entrenched. The test is judged on what exists now, so the mark is a Pass, earned by the base rather than the fabric.

Where the cash goes before it reaches the owner

Cash conversion asks whether all this growth actually reaches the owner, or whether working capital, capex, financing and dilution soak it up on the way.

Astera passes on the same logic that earned Credo the mark, with the same watch item attached. Operating cash flow was $74.6 million in Q1, up roughly sevenfold from a year earlier, against $7.6 million of capex, so free cash flow was firmly positive and the business funds itself. It holds $1.18 billion in cash and marketable securities and leans on no one. The cash balance was flat on the quarter only because $65 million went to the aiXscale deal, which is investment rather than burn.

The watch items are the ones that trail every richly paid semiconductor name, and they should never be netted away under a non-GAAP headline. Stock-based compensation ran $48.9 million in the quarter, close to $195 million annualized and about 16% of revenue, while the diluted share count drifts from 181 million toward a guided 184 million.

The standing cost to the owner is dilution. Two smaller flags sit next to it. Receivables jumped $51.8 million, faster than revenue, which is worth watching given the customer concentration, and GAAP net income got a lift from a one-off $6.9 million tax benefit that will not repeat. None of it breaks the Pass, but all of it qualifies it.

What the price has already decided

Price gets its own column, because what a business is worth and what you pay for it are two different facts.

The stock trades around $380 as of June 26, a market value near $68 billion, off an all-time high of about $441 set on June 22 when it joined the Nasdaq-100. That is well above the average analyst target near $264, on a trailing multiple close to 270 times earnings, a forward multiple still north of 100 times earnings, and about 40 times forward sales.

Read it for what it is. The market has folded the confirmed core and an on-time, in-full version of the whole developing roadmap into one number, the scale-up fabric, the optical transition and the custom pipeline all landing close to schedule, with very little room left in between. The June pullback is a smaller, separate matter. The high came on the inclusion date, when passive funds had to buy whatever the price, and some of that bid has drained back out since, a reminder that an index-driven peak reads the flows better than it reads the business. What you are paying up for is the part Astera still has to prove, sitting on top of the part it already has.

I am not going to pin an exact figure without a fresh primary-source read, but the posture is the most demanding the board uses, the kind where a strong print can still sell off, simply because the price got there before the business did.

The card

Tier: Confirmed. Astera clears all three conditions of the floor. The economic capture is visible today rather than promised. The replacement difficulty is proven today, through COSMOS and the Aries installed base. And the thing that makes the company hard to replace ships now rather than waiting in the roadmap. The placement rests on the incumbent signal conditioning and software franchise. The Scorpio fabric, the optical roadmap, UALink and the custom wins are the developing extension stacked on a confirmed core, the same shape as Credo, where the confirmed copper carried the grade and the optical was the part the price had chosen to believe. The two Partials, on supply control and demand commitment, are what keep this off a clean five, and a reminder that the base is doing the load-bearing work while the fabric is still to come.

Quarterly direction: Strengthened. Q1 beat on revenue and EPS, the Q2 guide is up 15% to 18% sequentially, a second custom CXL and KV cache design win came in, aiXscale and the new Israel Design Center are folded in, and the UALink customers went from abstract to named, with Amazon and AMD pointing at 2027. The business moved forward on every line that ships. The one thing that would have eased the price discipline did not. The valuation strengthened right alongside the business.

Price: The confirmed core and a flawless roadmap, folded into one number. About $380 as of June 26, a market value near $68 billion, off an all-time high of about $441 on the June 22 index-inclusion date, well above the average analyst target near $264, on a forward multiple north of 100 times earnings and around 40 times forward sales. The multiple is rich because the market has already folded the part Astera has proven together with a near-perfect version of the part it has not, and left almost nothing in between.

What could prove this wrong

The cleanest bear case has nothing to do with AI connectivity demand drying up. It is about capture. The rack-architecture layer goes to the larger platform vendors, or to hyperscaler internal designs, or to standards where Astera takes part without owning the economics, and Astera settles back into being a very good signal-conditioning company. That still leaves a strong business. Just a smaller one than the current multiple wants.

That risk is hiding behind two of the marks above. The fight on the fabric layer is about architecture as much as product, and the custom work sits partly inside stacks, NVLink Fusion among them, where a larger platform owner holds the leverage over economics and timing. Astera could keep growing through all of it and still end up with less strategic power than the price assumes. None of that shows up in the numbers today, which is exactly why it belongs in the price column rather than the grade.

When this is a position worth taking

A tier is not a recommendation, and Confirmed least of all means buy. A business can be Confirmed while its stock is paying a 2026 price for a 2028 outcome. Two different facts, kept in two different columns on purpose. The basket holds Astera, and the reason is the confirmed core, the connectivity layer the rack cannot be built without, showing up cleanly in margin and content per accelerator. That part I am happy to own at almost any sensible price.

What needs a view is everything the multiple adds on top. Buy Astera here and you are underwriting the scale-up fabric ramp, the optical transition and the custom pipeline all arriving close to the schedule management has laid out, at a price that has already taken most of the cushion out. Very little of that multiple is payment for the franchise Astera has already proven.

If you want the proven economics with a margin of safety, the straight answer is that the business is Confirmed while the entry is expensive, and waiting for a reset is a fair way to play it. If you are happy owning the architecture story before it fully ships, and you can stomach the swings a high-beta, index-driven name throws off, the confirmed core is the floor under that bet. The grade’s only job is to be precise about which part you are buying.

Since I already hold it, my own version of that is specific. I would get more willing to add on two triggers. A reset in the stock with the confirmed core still intact, or Scorpio, optical and custom starting to convert into revenue without margins slipping. Short of one of those, holding and adding are different decisions, and right now this is a hold.

What I am holding the placement against

A tier is a claim I have to be able to defend if the evidence turns. For Astera the triggers are mechanical, and I am setting them in advance.

Holds Confirmed as long as: the signal conditioning franchise keeps its margin and content trajectory, COSMOS stays embedded across the portfolio, and gross margin climbs back off the warrant-hit Q2 guide as the mix normalizes. The tier never rested on the fabric, so it does not hang on the fabric arriving on time.

Direction weakens if: Scorpio X, the flagship 320-lane part specifically, slips its second-half volume ramp, or Scorpio fails to become the largest product line by year end, with X overtaking P the way the CFO framed it. That would not break the tier. It would turn the developing extension from converting back into waiting, and it would sting most because it is the part the price has already paid for.

Tier breaks if: the evidence starts to undermine the base rather than the roadmap. A real crack in the 76% gross margin that is not mix or warrant, a loss of COSMOS incumbency to a rival layer, or retimer economics rolling over would pull the load-bearing marks out from under Confirmed. Nothing this quarter points that way.

The next real datapoint is the Q2 call in August, read against what Broadcom, Marvell and the hyperscaler capex prints say about the rack around it. Until then the placement holds, a Confirmed core carrying a developing roadmap.

Astera is one of the easiest companies on the board to admire, and one of the hardest to add to at today’s price. Those two things sit together on purpose. The whole point of the scorecard is to keep the business score and the price column apart.

Disclosure: The Best Ideas 2026 basket is ten equal weighted positions: Nvidia, Broadcom, Cadence, Vertiv, Powell Industries, Eaton, Arista, Credo, Astera Labs and Micron. The basket holds Astera Labs. Family account positions are disclosed separately when relevant. This is my own research and personal opinion, not investment advice. Do your own work before acting on anything here.