Credo, Graded

The first name on the board. Five business tests and a price column, every mark tied to a line in the filings, and the verdict held back until you have seen what earns it.

The scorecard needs a first name, and Credo earns it. The company just reported, the receipts are fresh, and the basket holds it, so it is the name I owe the first full audit. The grading exists to separate confirmed winners from stories standing close enough to the theme to catch some light. Credo is also a useful first test of the framework, because it has visible economics, a real technical position and a valuation that demands more than the latest quarter has yet proven.

Credo Technology Group sells the parts that let the machines inside an AI cluster talk to each other, copper and optical interconnect rated up to 1.6T. The established business today is built around the Active Electrical Cable, the ZeroFlap AEC that carries short-reach links inside a rack and across nearby racks, and around Credo’s own SerDes, the signal-integrity technology it designs in-house and reuses across every product. From there the portfolio expands, outward into optical DSPs, ZeroFlap optical transceivers and silicon photonics, and inward toward the silicon through retimers and the OmniConnect memory line, with the PILOT telemetry software watching the links once they are deployed.

The customers are mostly hyperscalers and neoclouds, and in fiscal 2026 the business produced $1.3 billion of revenue. On the board it sits in the interconnect layer, copper moving into optical, which is the seat the rest of this card sets out to test.

The setup is familiar to anyone who watched the print. Credo reported a quarter that should have made the stock easier to own, with revenue up 157% year over year to $437 million, non-GAAP gross margin of 68.3%, and free cash flow of $177.5 million, and the market sold it. The reaction is a price story rather than a business story, and the board is built to keep those two facts in separate columns. So the question is not whether the quarter was liked. It is whether the evidence in the filings earns Credo the tier I am about to give it.

Whether the growth turns into economics

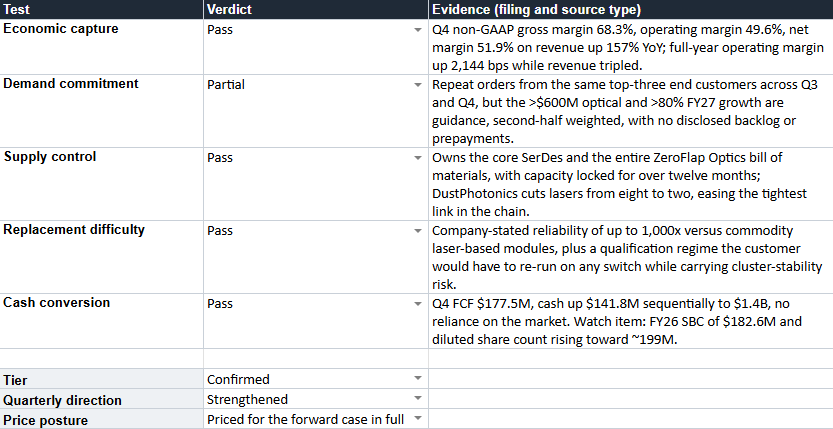

Economic capture asks whether growth turns into stronger economics rather than just more revenue, and Credo answers it without requiring any generosity from me. Q4 non-GAAP gross margin was 68.3%, operating margin 49.6%, and net margin 51.9%, on revenue that grew 157% year over year. Across the full year, operating margin improved by 2,144 basis points while the company tripled its top line, because operating expenses grew far slower than revenue.

That combination is the actual evidence. Plenty of companies in AI infrastructure can show demand. What is rare is a business that keeps more of every dollar as it scales, and Credo did exactly that while holding a gross margin in the high sixties. It is a clean Pass, and the least interesting line on the card, because it is the part nobody disputes.

How much of the demand is committed

This is the test where I have to mark Credo down, and it is worth being exact about why. Demand commitment asks how much of future demand is underwritten by something binding, whether backlog, prepayments, purchase commitments, or repeated production orders, rather than by management confidence. The proven part is real. The same top three end customers anchored both Q3 and Q4, which is the repeated-order evidence the test rewards.

But the part the story now turns on is the fiscal 2027 case, more than $600 million of optical revenue with each of three legs above $100 million, driving more than 80% total growth, and that case rests on guidance rather than disclosed commitment. Brennan was candid that the company has been in demand-generation mode for about six months and locking in supply for twelve. Read carefully, that is Credo committing to its own suppliers, not customers committing to Credo. There is no backlog figure, no prepayment, and the concentration is heavy, with the largest customer at 34% of Q4 revenue. None of this says the demand will not arrive. It says the demand is credible and forecast rather than contracted, and the test is built to hold that line, so the mark is Partial rather than Pass.

The scarce thing the company owns

Supply control is the test that catches a company riding a hot theme while the bottleneck sits in someone else’s hands, and it is where Credo separates from the names that merely sell into the same end market. The thing Credo owns is its SerDes, and on the Bank of America stage Brennan was direct that the SerDes is what unlocked the entire opportunity, the core technology that lets the company build optimized silicon, then a system-level product, then wrap it in firmware and telemetry software. That vertical position is not a slogan.

On the ZeroFlap Optics ramp the company owns the entire bill of materials, has been locking in supply for more than twelve months, and secured capacity commitments by leaning in ahead of demand. The DustPhotonics architecture cuts the laser count from eight to two, roughly a 75% reduction, which matters because lasers are the tightest link in the optical chain. A supplier that can ship more reliably into a constrained chain controls something a competitor cannot copy on a roadmap slide, which is what a Pass on supply control is supposed to capture.

What breaks if the customer leaves

Replacement difficulty asks what gets harder, slower, or more expensive for the customer who switches away, and the answer for Credo is concrete enough to be uncomfortable for any would-be challenger. The ZeroFlap products claim up to 1,000 times the reliability of commodity laser-based optical modules, and in a cluster the first links from GPU to switch carry no redundancy, so a single unstable link can take the whole system down. Brennan described the qualification work in physical terms, more than twenty thermal chambers in Taiwan running a customer’s own switches and NICs at full speed, varying temperature and voltage and power cycling until the link breaks, then engineering it until it stops breaking. The customer receives that qualification data, and by management’s account the company has not failed one of these qualifications.

That is the switching cost in plain form. A buyer does not simply swap a part. The buyer re-runs that entire validation and accepts cluster-stability risk measured in idle GPU time sitting on billions of dollars of capex, which is the switching cost that earns the Pass.

Where the cash goes before it reaches the owner

Cash conversion earned its place on names where the revenue looked wonderful and the cash never arrived, so it deserves a careful read even on a business this profitable. The headline is clean. Q4 free cash flow was $177.5 million, cash rose $141.8 million sequentially to $1.4 billion, and the company funded a large inventory build while still growing the balance sheet without leaning on the market. If Credo were stuffing the channel ahead of soft demand, the cash flow would not look like this, so the test passes.

The asterisk is dilution. Stock-based compensation ran $182.6 million for the full year, and the diluted share count is climbing toward roughly 199 million in the first quarter of fiscal 2027. That does not break the test, because the cash genuinely converts and reaches the balance sheet, but it is the line where an owner gives back a slice of the economics on the way through. Dilution is material, but it is not yet absorbing enough of the operating leverage to overturn the underlying cash conversion, so it belongs on the watch list rather than in the verdict, and the test passes.

The bear case the tier has to survive

The tier has to survive the standard argument against Credo, which has always been that copper wins today but optical eventually displaces the opportunity. That risk matters less now, because Credo is participating in both sides of the transition rather than betting on one. It sells the copper, it is ramping optical DSPs and ZeroFlap Optics, and through DustPhotonics it now holds silicon photonics with a stated path to CPO and NPO.

The old fear was disruption by the optical shift. The evidence points toward participation in it instead, which lets the placement rest on the copper business while the optical extension develops on top.

What the price has already decided

Price keeps its own column because what a business is worth and what you pay for it are different facts, and Credo is a clear illustration of why the separation matters. A strong print sold off, which by itself says more about the entry price than about the quarter. The posture I read is the most demanding of the three the board uses. The price is set for the forward case to be delivered in full, not merely for the current path to hold.

Here the card folds back on itself in a way worth sitting with. The single test Credo could not fully clear, demand commitment, concerns the fiscal 2027 ramp that sits on guidance. The price assumes that same ramp arrives on time and at scale. So the one place the evidence stops short is the place the valuation has already paid up. That is not a contradiction inside the company, it is where the risk sits.

The card

Tier: Confirmed. Economic capture is visible today, and both supply control and replacement difficulty are proven in the copper business that ships now rather than in the roadmap. Optical is the developing extension on top of a confirmed core.

Quarterly direction: Strengthened. Optical moved from optionality into fiscal 2027 revenue guidance, DustPhotonics closed and added silicon photonics with a path to CPO and NPO, and the supply-control evidence grew more concrete. The business strengthened while the stock fell.

Price: Priced for the forward case to be delivered in full. A strong print sold off because the price had moved ahead of the quarter.

What I am holding the placement against

Credo earns Confirmed, and a tier is a claim I have to be able to defend if the evidence turns. The copper business proves the moat today, and the optical business is the developing extension the price has already chosen to believe. The question I will hold the placement against is whether the fiscal 2027 optical ramp arrives in the second half as delivered, repeatable revenue at the guided scale, with gross margin still in the high sixties.

If the ramp slips, the quarterly direction weakens and the demand-commitment Partial stays open, but the tier holds, because it was never resting on the optical case. Confirmed only breaks if the evidence starts to undermine the copper economics, the supply control or the replacement difficulty that earned it.

Click here to see the complete scorecard

Disclosure: The Best Ideas 2026 basket is ten equal weighted positions: Nvidia, Broadcom, Cadence, Vertiv, Powell Industries, Eaton, Hubbell, Arista, Credo and Astera Labs. The basket holds Credo. Family account positions are disclosed separately when relevant. This is my own research and personal opinion, not investment advice. Do your own work before acting on anything here.

All figures are drawn from Credo’s fiscal Q4 2026 press release and financial statements, the Q4 2026 earnings call, and the company’s Bank of America 2026 Global Technology Conference appearance. Hard numbers are primary filings; forward figures are management guidance and are labeled as such.