IQE, Graded

A real position in the bottleneck, still unproven in its own numbers.

Key takeaways

The whole InP optics chain is now reporting the bottleneck in its own numbers, from substrate backlogs and tool orders to component margins and module capacity. IQE sits in the epitaxy layer the chain runs through.

IQE is the upstream way to play the AI optics constraint, one layer below the transceivers and components most investors watch. It grows the indium phosphide epiwafers the high-speed lasers are built from.

The validation turned concrete in the last two months. MACOM invested £45m and took a board seat, Tower signed a multi-year InP epiwafer agreement, and an £81m raise took IQE off a formal sale process.

The stock has already rerated hard on that validation, which raises the bar for what the next set of results has to show.

The open question is whether any of this has reached IQE’s own numbers yet. How it grades across the five business tests, and where that leaves the name, is below.

IQE is the first name on this board that does not make a finished connectivity product. It sits below the transceiver layer, in the epitaxy used to make the photonic devices, the lasers, modulators and photodetectors, that can end up inside transceivers and optical systems, which is exactly why it is worth grading. The scorecard has so far looked at the component and module layer, Credo and Applied Optoelectronics. IQE tests whether the same five questions hold up one step deeper, in the qualified epiwafer layer the optics industry needs before lasers and photonic devices can scale.

The setup is unusual. For most names on this board the demand evidence and the company’s own results move together, and with IQE they have pulled sharply apart. The chain around IQE has spent the last two months reporting the indium phosphide constraint directly in its order books and its margins. IQE’s own FY2025 numbers, reported on 28 May, show a company whose revenue fell and whose profitability halved. The interesting part of this card is that gap, and whether the framework can tell the difference between a real position on the critical path and a turnaround that simply happens to sit near a hot theme.

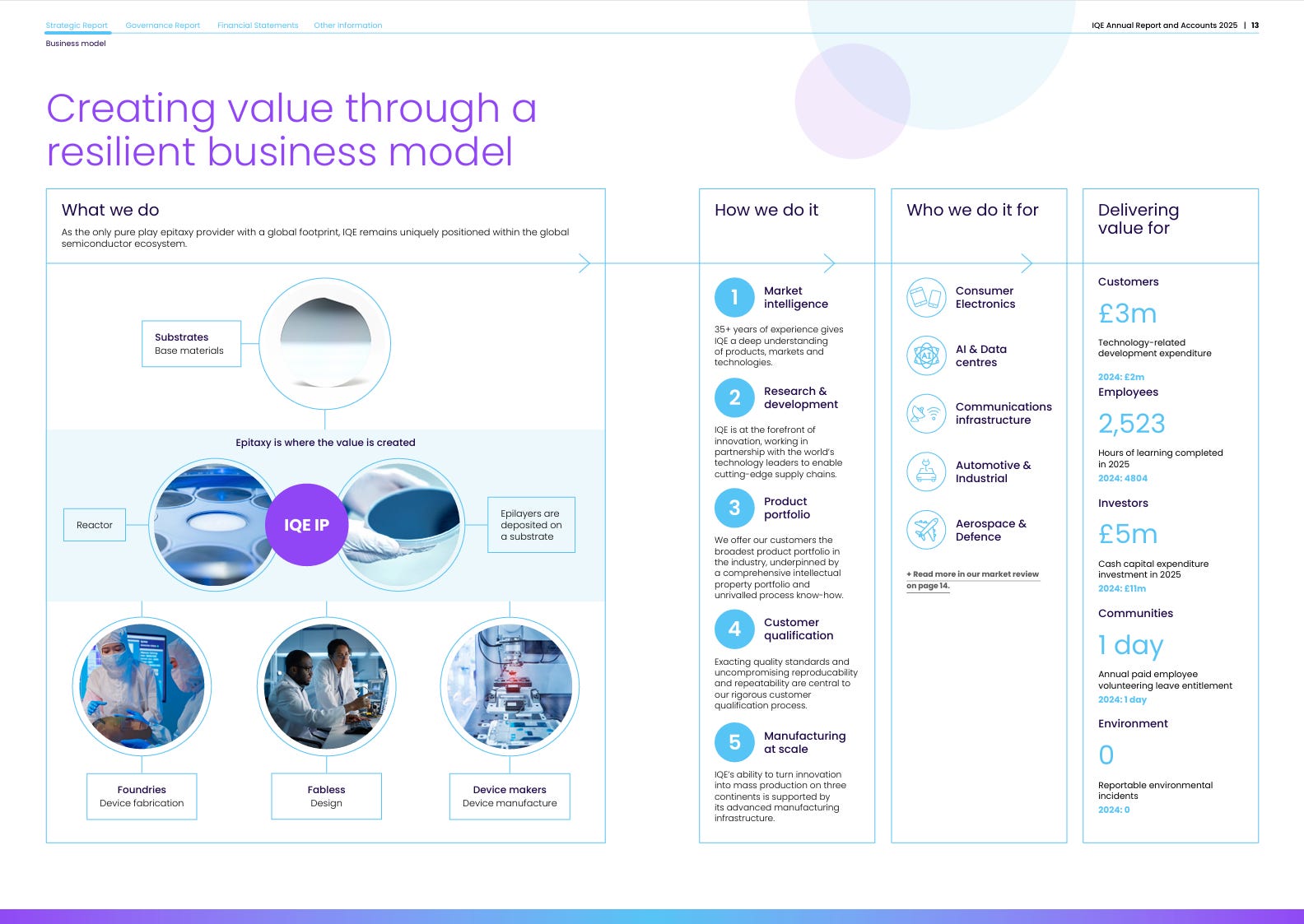

What IQE does is grow compound semiconductor layers, mostly indium phosphide, gallium nitride and gallium arsenide, on base substrates, which device makers then turn into lasers, photodetectors, modulators and sensors. The material that matters for this board is indium phosphide, the basis of the high-speed lasers inside optical transceivers. As AI clusters grow, more of the data movement shifts toward optical links. Many of the highest-speed datacenter links rely on lasers and photonic components where qualified InP epitaxy becomes a critical part of the manufacturing chain. IQE has done that epitaxy for decades, across multiple sites, which is the entire reason it is in this conversation despite financials that, on their own, would not earn a second look.

So the tier is withheld until the marks are in, and the marks settle one question. The bottleneck looks real, and the chain now gives enough evidence to treat it seriously. The question is whether IQE captures any of it, and that is what the filings have to show.

What the companies around IQE are now reporting

Start with the layer directly beneath IQE. AXT makes the indium phosphide substrate that epitaxy is grown on, and its Q1 2026 print, reported 30 April, is the clearest single datapoint in the chain. InP revenue was $13.6 million, more than half of the company’s total $26.9 million, and management put the InP backlog above $100 million for the first time, up from more than $60 million a quarter earlier. Non-GAAP gross margin moved to 29.9% from 21.5% the prior quarter. AXT raised $632.5 million and committed it to doubling InP capacity in 2026 and again in 2027, while moving toward six-inch wafers. These are reported numbers, drawn from primary filings. When the substrate layer is this tight and raising capital to double twice, the constraint is structural rather than a passing module-level story, and it sits underneath IQE. That tightening is evidence about the chain rather than proof that IQE itself is winning business.

At the equipment layer, Aixtron tells the same story from the capex side. Its Q1 2026 order intake was €171.4 million, up 30% year-on-year, and optoelectronics made up roughly €118 million of that, close to 70% of the total, even as revenue fell 47% to €59.4 million at the trough of the equipment cycle. Management named the cause directly, laser-related datacom demand, with its G10-AsP platform taking the majority of volume orders for the EML and PIC-based lasers going into AI infrastructure. The detail worth holding is that most tools were ordered for four-inch wafers but already fitted with six-inch conversion kits. The industry is tooling up for a larger capacity phase rather than squeezing the existing lines, and it is doing so now.

Move up to the components and the bottleneck stops being an order book and becomes an income statement. Lumentum’s fiscal Q3, reported 5 May, showed revenue of $808.4 million, up 90% year-on-year, with non-GAAP gross margin of 47.9% and non-GAAP operating margin of 32.2%, and it guided the next quarter to between $960 million and $1.01 billion. On the call management said components and laser chips were effectively sold out, its Japanese wafer fab was fully allocated, and the supply-demand gap on EMLs and pump lasers was running above 30%. It acquired a fifth indium phosphide fab in Greensboro for capacity that will not even contribute until early 2028. Coherent, from the other large photonics platform, was blunter still, calling indium phosphide an industry-wide constraint and saying it expects to double its six-inch InP output by the end of this calendar year, a quarter ahead of plan, and more than double it again by the end of 2027. Its datacenter and communications revenue grew more than 40% year-on-year. Two of the most important photonics platforms in the market are saying the same thing, in revenue, in margin and in capex.

At the module layer, Applied Optoelectronics, the name graded last on this board, confirms the demand is outrunning capacity rather than merely existing. Its Q1 revenue was a record $151.1 million, it shipped its first 800G volume to a hyperscaler and took a first 1.6T order, and it said demand for 800G and 1.6T modules should exceed its production capacity through the middle of 2027. AAOI also carries the cautionary half of the lesson, because its non-GAAP gross margin was 29.2% and it is still losing money, proof that being inside the right market does not by itself produce good economics. That qualifier matters more for IQE than the demand does.

LandMark Optoelectronics is the most useful comparison I found. It sits close enough to the laser epitaxy, laser diode and silicon photonics component layer to serve as a useful control case for what the economics can look like when AI optics demand reaches that part of the chain. Its FY2025 results show revenue up about 82% to NT$2.20 billion and net income swinging from a loss to NT$428 million, with earnings per share of NT$4.66 against a small loss the year before, driven by AI and data center shipments and a sharp ramp in silicon photonics products. That is the shape IQE bulls are hoping to eventually see. It shows what the layer is capable of, and what IQE does with the same opportunity is the question the card takes up.

The last and most direct receipt is Tower Semiconductor, because Tower is now a named commercial customer for IQE’s InP epiwafers. On 15 June the two signed a multi-year agreement for IQE to supply InP epiwafers into Tower’s silicon photonics platforms, covering 200 gigabit per lane pluggable transceivers, prototyping of 400 gigabit per lane modulators, and optical circuit switches. Tower’s own Q1 filing gives useful context for the scale building around its silicon photonics platform, $1.3 billion of contracted silicon photonics revenue for 2027 from its largest silicon photonics customers and $290 million of prepayments from those customers in a single quarter. That figure is context for the platform rather than a measure of IQE’s own opportunity. IQE is a named supplier into the roadmap, with the size of its own share still to be disclosed.

Put the chain in one line and it reads cleanly. Substrate tightening and doubling capacity twice, tools booked for laser datacom, two component platforms reporting the constraint in their margins, the module layer short of capacity into 2027, a nearby control case already earning the economics, and a foundry customer with a billion-dollar photonics book signing IQE to supply it. The direction of demand is not in question. What follows is whether IQE turns any of it into a cleared mark.

What the numbers did while the story improved

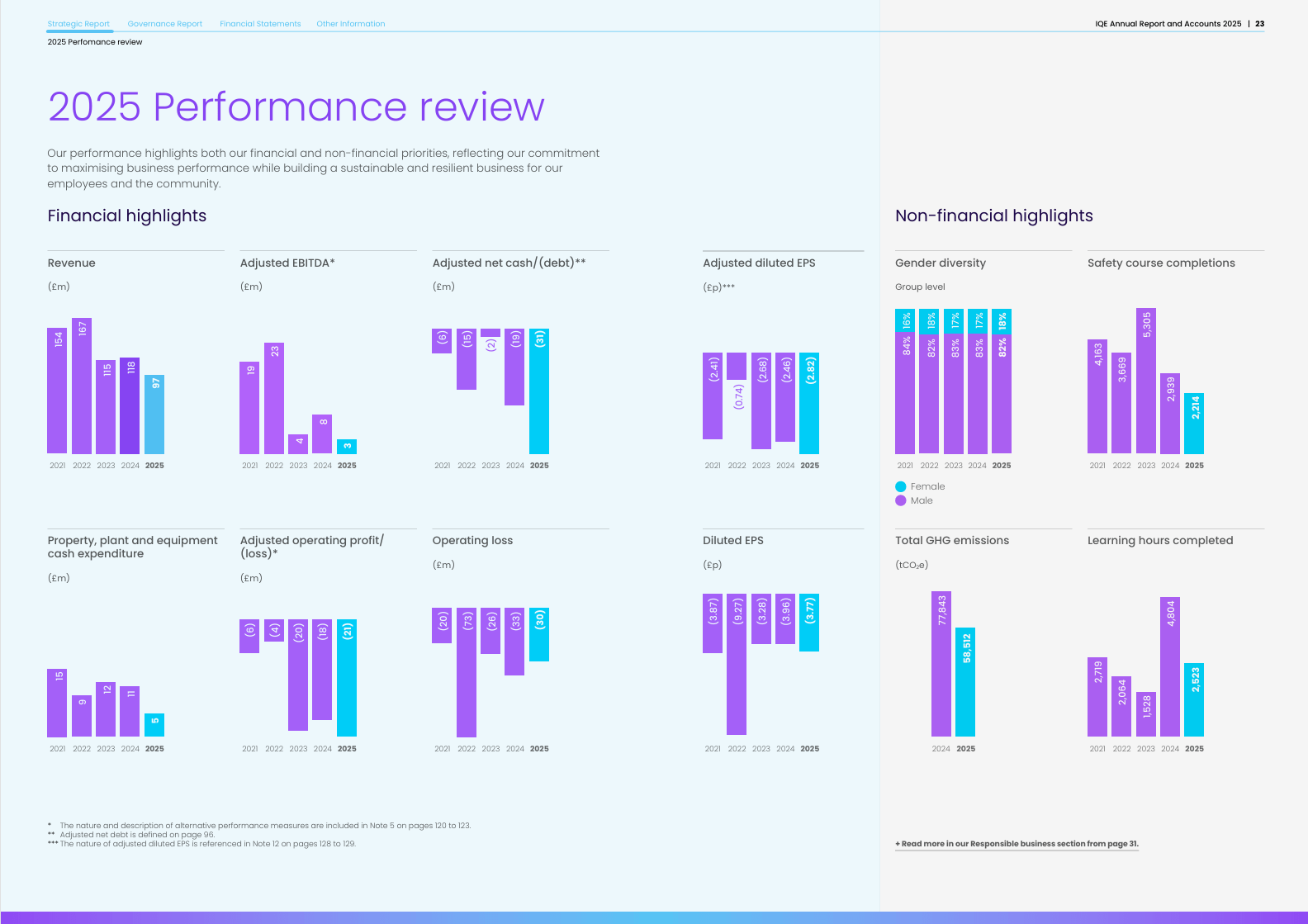

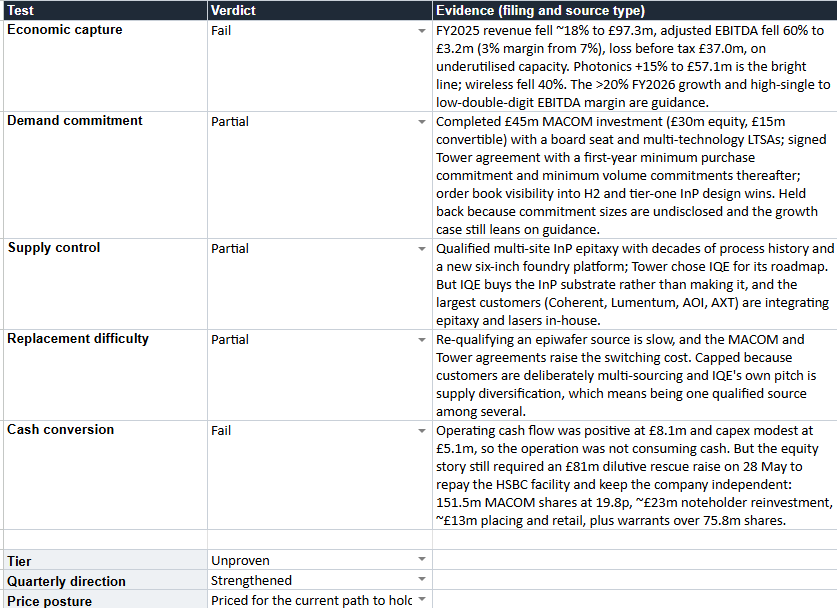

Economic capture asks whether growth turns into stronger economics rather than just more revenue, and IQE’s FY2025 results answer in the wrong direction. Revenue fell to £97.3 million from £118.0 million, a drop of about 18%. Adjusted EBITDA fell 60% to £3.2 million, taking the margin to 3% from 7%. The reported loss before tax was £37.0 million, though much of that is non-cash, with depreciation and amortisation on a large asset base the main driver, so the headline figure overstates the cash strain. The split underneath was the one bright line, photonics revenue rose 15% to £57.1 million on InP demand for AI and data centers, while wireless fell 40% to £40.1 million on weak handsets and inventory. The reason the chain’s bottleneck has not yet reached IQE’s bottom line is in that split. The InP demand the rest of the chain is reporting has already turned up in IQE’s photonics line, which grew second-half weighted, but photonics is the smaller half of the business and the 40% wireless collapse swamped it. IQE also sits a step upstream of the module makers carrying the constraint in their 2026 prints, so it likely captures the same demand differently: earlier in the manufacturing chain, at lower unit value than the finished module, and with timing that depends on customer qualification and production ramps. The recent acceleration has not had time to flow through at scale. Management attributes the EBITDA fall to a lower revenue base and the underutilisation of its manufacturing assets, which is the honest description of the problem. The capacity exists, the volume to fill it does not yet, and that is the whole question for the cost base. The photonics line already shows the fixed base producing leverage when volume arrives. The drag is the wireless half, where the same capacity sits underused.

Whether the next print reads as operating leverage or as stranded capacity depends on which force wins as InP scales. The forward case, guidance for more than 20% revenue growth in FY2026 and a high-single to low-double-digit EBITDA margin, is exactly that, guidance, and the test only credits results. On the reported numbers this is a Fail, and it is the clearest mark on the card.

IQE has also put a clearer timeline around the proof than the current share-price debate sometimes suggests. It is guiding to more than 20% revenue growth in FY2026, with strong order book visibility into the second half and a high-single to low-double-digit adjusted EBITDA position. In its going concern base case, management refers to Board-approved forecasts for FY2026 and H1 FY2027 that assume revenue growth of at least 20% across both, consistent with guidance and current analyst consensus. That gives the proof a bounded window rather than an open-ended wait, and it means no single quarter has to carry the whole verdict. H1 2026 should show whether the turn has started, H2 2026 whether the order book is converting, and H1 FY2027 is where IQE’s own base case still assumes the growth continues.

How much of the future is signed

Demand commitment asks how much of future demand is underwritten by something binding rather than by confidence, and this is the test where IQE scores best, which is itself the story of the card. Two things here are already signed. MACOM has completed a £45 million strategic investment, £30 million of equity and £15 million of non-interest-bearing convertible loan notes, taken a board seat, and entered long-term supply agreements across multiple technologies. A customer putting in real money, taking a board seat and signing supply agreements at once is securing its supply chain. The Tower agreement is more concrete still on the demand side, with a minimum purchase commitment from Tower in the first year, a reciprocal supply commitment from IQE, and minimum volume commitments thereafter. Alongside that, IQE reports strong order book visibility into the second half and multiple tier-one InP design wins.

What holds the mark at Partial rather than Pass is magnitude. Neither the MACOM supply agreements nor the Tower commitments have disclosed sizes, so the binding demand is real in form but unquantified, and the FY2026 growth figure the equity now leans on is still guidance. Two signed agreements with strategic counterparties is a stronger demand base than most names carry at this stage, and it is the closest IQE comes to clearing a test. It also speaks to the question those agreements raise, whether IQE is being signed for pricing power or merely as useful second-source capacity. The structure leans toward the former, since a disposable backup supplier does not usually attract equity, a board seat and a reciprocal commitment, and Tower chose IQE specifically for its roadmap. Without disclosed margin, volume and duration, though, the agreements show strategic necessity more than pricing power, and that gap is exactly why the mark is Partial rather than Pass.

Whether IQE controls the scarce thing or sits beside it

Supply control is the test that separates owning a bottleneck from standing next to one, and for IQE the answer cuts both ways. What IQE controls is qualified, high-volume InP epitaxy across multiple sites, with decades of process history and a newly launched six-inch foundry platform aimed at silicon photonics. Qualification at this layer is slow and customer-specific, which is a real barrier, and Tower choosing IQE for its roadmap is evidence the expertise has value a customer will pay to secure. The layer below it is another matter. IQE buys the indium phosphide substrate rather than making it, which is the part AXT and Sumitomo sit on, and AXT’s own results show that layer is the tighter constraint right now.

The harder problem sits above IQE. The same chain that validates the demand also shows the largest players integrating the epitaxy in-house, and merchant epitaxy is the link most exposed to a customer deciding to build rather than buy. The real risk is subtler than InP demand drying up. The strongest integrated photonics platforms are solving more of the constraint themselves, which leaves outsourced epitaxy with strategic relevance and less of the long-term pricing power.

Coherent is the clearest case. It has called indium phosphide an industry-wide constraint, it is doubling internal InP output a quarter ahead of plan and plans to more than double it again by the end of 2027, and its six-inch platform is already producing EMLs, CW lasers and photodiodes at yields above its three-inch lines, with the first transceivers built on those lines already contributing to revenue and gross margin. Lumentum is adding InP fab capacity in Greensboro and pulling more of its own laser supply into the 1.6T ramp. AAOI is expanding its in-house laser and InP capacity. Aixtron’s order book, with six-inch conversion kits already fitted to the tools, shows the same direction from the equipment seat. The industry is buying more supply and, increasingly, building more of the bottleneck itself.

That does not make IQE irrelevant, and the MACOM and Tower agreements push back, showing that qualified, outsourced epiwafer capacity still carries strategic value. But it changes what has to be underwritten. IQE’s strongest realistic role may be as a qualified external supply and diversification layer for customers that want geographic resilience and proven epitaxy without building everything in-house, rather than as the primary owner of the InP profit pool. If merchant epitaxy becomes mainly bridge capacity while the largest customers internalise the highest-value work, IQE can be important to the ecosystem and still disappoint shareholders. That tension, between a real qualification barrier with signed customers and a profit pool being built in-house by the players best placed to take it, is exactly why the mark is a Partial.

What switching away would cost

Replacement difficulty asks what gets harder for a customer who leaves, and the honest answer sits between the two forces in the supply-control mark. The friction is real. Re-qualifying an epiwafer source is slow, and Tower and MACOM have just locked themselves into IQE with agreements that would be expensive to unwind, which is the clearest replacement cost IQE has. Against that, the structural pull of the chain is toward customers reducing their dependence on any single external supplier, and IQE’s own pitch is supply diversity and resilience, which by definition means being one qualified source among several rather than the only one. A customer that picks IQE partly to avoid depending on any single supplier has little reason to feel stuck with it. The qualification cost is real and the recent agreements raise it, so this is a Partial, but the same insourcing dynamic that caps supply control caps this mark too.

What the balance sheet needed before any of this

Cash conversion asks whether growth turns into cash for the owner or whether capital intensity and dilution absorb it first, and IQE’s recent history answers plainly. Before any of the demand could be pursued, IQE had to raise £81 million, completed on 28 May, to repair a balance sheet that had been the subject of a formal strategic review, advised by Lazard, that included a possible sale of the whole company. The raise repaid the HSBC revolving credit facility and steadied working capital, and it was heavily dilutive. MACOM took 151,515,151 new shares at 19.8 pence for about 11.5% of the votes directly, existing noteholders reinvested roughly £23 million at the same price, a placing and retail offer added around £13 million, and MACOM also holds the convertible notes and warrants over a further 75,757,575 shares, which are alternative rights to the same shares and lift its total notified interest to 14.7%. The owner’s slice was diluted substantially to keep the company independent and funded. Adjusted net debt was £31.5 million at the December year end, and the raise then repaid the HSBC facility and produced net cash inflows of about £27.9 million. The immediate balance sheet risk was reduced, not eliminated.

There is a fair counterpoint, and the test should credit it. IQE’s reported net cash flow from operations was positive at £8.1 million, up from £1.3 million, helped by working capital, and cash capital expenditure was modest at £5.1 million. The operating engine was not burning cash. But the equity story still required rescue financing rather than internally generated capital, and the per-share economics were diluted on the way through, which is what the test measures. That makes it a Fail, with the qualifier that the failure was a balance sheet that needed rescuing rather than an operation consuming cash at the AOI scale. The forward question is whether that rescue was a one-time bridge or the first of several. With the HSBC facility repaid, net debt modest and capex light, IQE looks able to fund incremental organic growth from the repaired balance sheet, which would make the dilution a bridge that paid for itself. The risk on the other side is that fully capturing the bottleneck, the six-inch foundry buildout and the InP capacity to match the chain, costs more than incremental, and the convertible and the MACOM warrants already sit over the equity as a standing dilution overhang. Whether shareholders keep that growth turns on timing: margins that land before the next capital call mean the raise was the whole cost, while margins that come later mean the layer thesis can be right even as the equity keeps paying for it.

The bear case the tier has to survive

The argument I would make against IQE myself is that it is a strategically useful merchant supplier that never captures the economics, and the recent history gives that case real weight. This is a company that was, until late May, in a formal sale process, with a full sale of the business and a separate sale of its Taiwan operations both on the table. The equity validation that followed came partly because the alternative was being sold. The customers now signing supply agreements and taking board seats are, in several cases, the same companies building internal capacity that could make merchant epitaxy less necessary over time. A supplier can be critical to its industry and still be the layer where margin does not settle, and IQE’s own long record of operating below where investors hoped is the evidence that importance has not historically converted into owner returns.

The rebuttal grants the bear its reading of the past and rests instead on the last two months, where the external validation is more concrete than anything before it, two signed agreements, an equity investor on the board, a foundry customer with a billion-dollar photonics book. That is why the name is worth grading at all. It is also why the grade lands where it does, because external validation, however concrete, does not stand in for a cleared internal test.

What the price has already decided

Price keeps its own column, because the business and the stock are different facts, and IQE is a sharp example. The shares have rerated enormously through 2026, up several hundred percent on the year on the combination of the AI optics narrative, the MACOM investment and the Tower deal, in a highly volatile name. The market has already taken the validation as the thesis. What the price is paying for is the conversion, the FY2026 growth, the rising utilisation and the margin recovery, which are precisely the internal proofs the card could not mark. A stock that has rerated on external receipts while the internal receipts are still outstanding is paying in advance for the part that has not arrived. I am not putting a precise multiple on it here without a fresh primary-source read, but the posture is the most demanding kind, priced for the conversion to be delivered.

The card

Tier: Unproven. IQE holds a real position on the critical path with the strongest external validation of any name at this stage, an equity investor on the board and a foundry customer signed. But it cleared no test to a Pass, and the two tests that measure the owner’s economics, capture and cash conversion, both failed on the reported numbers. AOI sits one tier higher at Developing because it has a single decisive Pass, the laser fab, doing the load-bearing work. IQE has no such mark yet. Unproven is the seat for a name where the evidence around the business is real and the evidence inside it has not arrived.

Quarterly direction: Strengthened. This is the first card, so it sets the baseline, and over the reporting window the case improved materially from the outside. The MACOM raise took IQE off the sale block and onto the board, the Tower agreement made it a named foundry supplier, and the surrounding chain reported the bottleneck more clearly than ever. What did not strengthen was the one thing that would move the tier, the internal numbers, which is why the direction is up while the tier stays low.

Price: Priced for the conversion to be delivered. The rerate has already taken the external validation as the thesis, leaving the price paying for the internal proof the card could not mark.

When this is a position worth taking

A tier is not a recommendation, and Unproven in particular describes a business you would be underwriting almost entirely on what has to happen next. For an investor who wants the bottleneck already visible in the owner’s numbers, the honest answer is the watchlist, because the print that would move this up is also the one that removes most of the guesswork, and the rules below say what it has to contain. The case suits a different appetite. For an investor who wants the upstream way to play the AI optics constraint and can wait out an unproven turnaround, IQE is a coherent way to own it, with strategic validation already behind it. The market has taken that as given, so what you are underwriting from here is the dilution, the insourcing question, and whether FY2026 carries it into IQE’s own numbers. The grade’s only job is to be precise: a real position on the critical path whose economics went backwards last year, with the proof of the turn still ahead.

What I am holding the placement against

Unproven is a claim I have to be able to revise, and the triggers are mechanical.

Moves to Developing if: FY2026 revenue accelerates in photonics and InP as guided, utilisation rises and adjusted EBITDA margin moves back toward the high single digits, and at least one of the MACOM or Tower commitments is disclosed with enough size to quantify the demand. That combination turns economic capture and demand commitment from words into evidence, and it is the print that would justify the rerate the stock has already had.

Stays Unproven if: revenue grows but margin and utilisation stay stuck, so the validation is real and the owner still is not capturing it. At that point the gap between the chain’s receipts and IQE’s own becomes the whole story, and no amount of external signing changes the tier.

Moves off the board if: the demand evidence reverses, the substrate constraint eases enough that customers internalise faster, or the company returns to needing capital. It also moves off if the next few reports suggest the MACOM and Tower agreements are functioning mainly as bridge capacity rather than durable outsourced supply, or if the largest photonics platforms keep internalising the constraint faster than IQE can turn its external capacity into margin and cash. The thesis rests on IQE being the qualified external layer the industry still needs, and if that need narrows, there is no mark left holding the placement up.

One caveat sits under the whole grade. The last hard read on IQE is FY2025, to 31 December, while the chain section leans on Q1 2026 prints, so IQE is being judged a quarter behind the companies around it. Close to two quarters have passed since that year end, and the events inside them, the May raise and the June Tower deal, point the same way without being financial results. Nothing reported since points the other way, and nothing yet shows the turn in a reported period.

The immediate waypoint is the annual general meeting on 30 June, with any trading commentary there the first update since the Tower deal. The first substantial print is IQE’s H1 2026 results expected in the autumn, read against the next quarter from AXT, Aixtron, Lumentum, Coherent and Tower. The broader evidence window runs through H2 2026 and into H1 FY2027, since IQE’s own base case assumes revenue growth of at least 20% across FY2026 and H1 FY2027. Until then the placement holds, an upstream position with a far stronger evidence base than it had a month ago, and not a single test yet cleared.

Disclosure: The Best Ideas 2026 basket is ten equal-weighted positions: Nvidia, Broadcom, Cadence, Vertiv, Powell Industries, Eaton, Arista, Credo, Astera Labs and Micron. I do not own IQE. A family account holds a starter position in Aixtron, which is mentioned in this piece. Family account positions are disclosed separately when relevant. This is my own research and personal opinion, not investment advice. Do your own work before acting on anything here.

Upstream isn't IQE are dependent on Chinese export permists on gallium and indium phosphide? Apparently the company is trying to "diversity sources". is this possible and within what timeframe?