Micron's Record Quarter

FQ3 2026, reported June 24, 2026

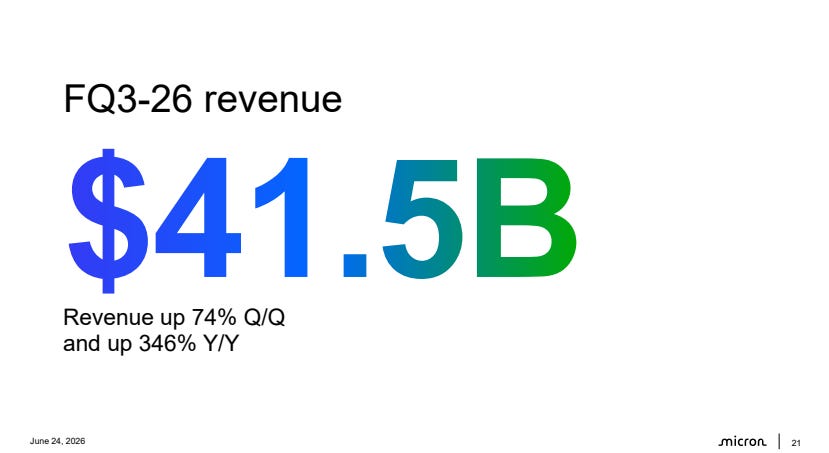

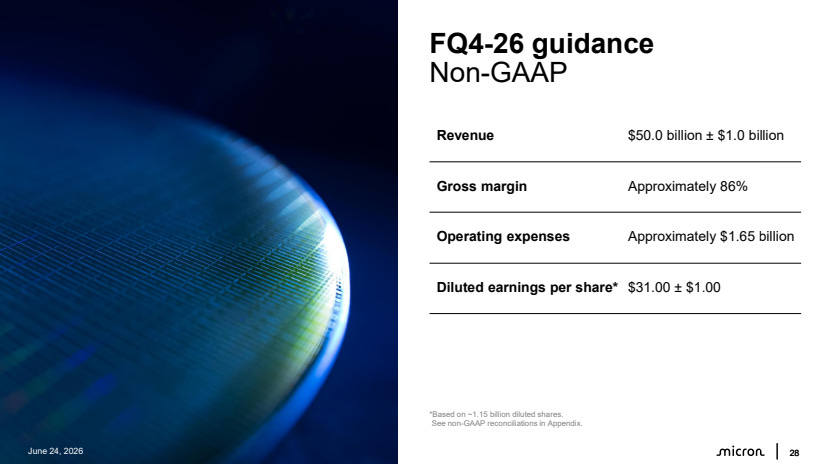

Micron printed a quarter that cleared every bar it set for itself. Revenue of 41.5 billion dollars, up 74 percent sequentially and 346 percent year over year. Non-GAAP gross margin of 84.9 percent. EPS of 25.11, all above the high end of guidance. The August quarter is guided to 50 billion in revenue and roughly 86 percent gross margin.

My instinct as an auditor is to check whether the headline matches the books before I get excited about it. With Micron it does. The revenue is real, the cash followed it, operating cash flow was 25.4 billion and free cash flow a record 18.3 billion. There is no narrative gymnastics needed to read this quarter. The one line I would keep an eye on is receivables, which sit at 31 billion against roughly 9 billion a year ago, with close to a 20 billion build over nine months. In most companies that would worry me. In Micron’s case it is the backside of booking a price spike into a concentrated, high quality customer base, so it is not alarming today. But it is the line that turns a price spike into a credit question if it keeps running, and I will follow it.

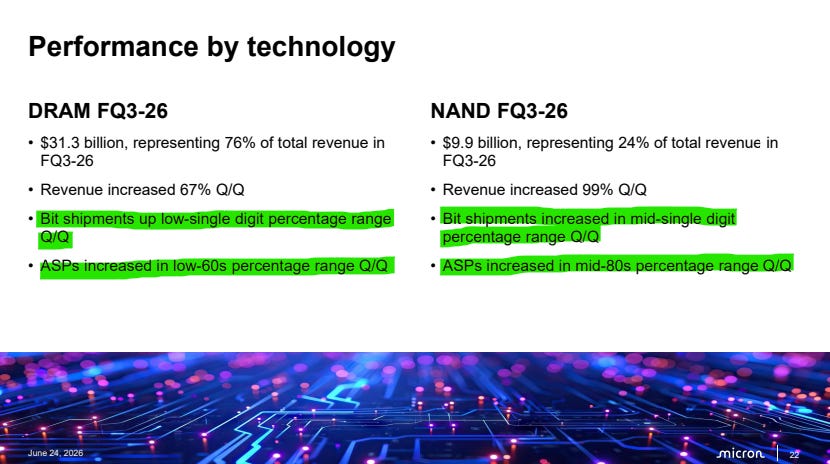

What I find more interesting is what the print says about the cycle. Almost all of the growth came from price. Look beneath the headline and bit shipments barely moved, DRAM up a low single digit percentage and NAND up a mid single digit percentage. Then look at average selling prices and they jumped, up in the low 60s percent range for DRAM and the mid 80s for NAND. So almost all of this growth was price. A real shortage does not look any clearer than this when it reaches the income statement. But the same numbers that make this a record also raise the question I think deserves its own treatment: are we looking at a company near the top of a pricing cycle rather than the start of one?

The structural news sits in the contracts

Micron has now signed sixteen Strategic Customer Agreements, five year take-or-pay contracts running through 2030, with remaining performance obligations of roughly 100 billion dollars across fourteen of the sixteen, and 22 billion in deposits and financial commitments, of which about 18 billion is cash.

Management framed the floor pricing inside these contracts as delivering gross margins above the company’s peak in any past cycle. By their own math the contracted floor covers around a quarter of revenue over the term, rising toward 40 percent as the remaining agreements complete. Hold the proportions, though. Three quarters of revenue still rides the cycle today, and the RPO figure is a minimum at minimum price, deliberately conservative, so it is a floor on the contracts rather than a forecast of revenue.

Things you might not catch on a first read

Some things I found interesting after reading through, that might not have been the focus in the other Micron report summaries out there.

They are deliberately not maximizing HBM. On the call Micron said it is holding HBM market share close to its overall DRAM share by choice rather than chasing it, because HBM consumes far more wafers per bit and taking maximum share would starve the rest of its supply. In a shortage the reflex is to grab all the high value share you can. Micron is leaving some on the table to protect deliveries to its broader customer base, which is also part of why it can credibly call tightness so far out.

The margin is near its mathematical ceiling. The Q4 guide lifts revenue more than 20 percent but gross margin only about a point, from 84.9 to roughly 86 percent. At an 85 percent margin, cost of goods is only 15 percent of revenue, so additional price adds almost nothing to the margin line, and the CFO said as much. From here the margin lever is mostly spent, and further expansion has to come from volume and factory absorption rather than price.

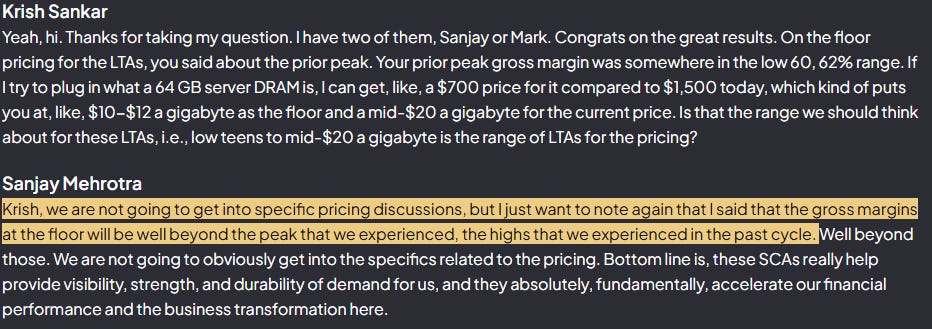

The contract floor sits near half of today’s spot. On the call, Krish Sankar of TD Cowen ran the numbers backward and landed on a floor of roughly half the price Micron is getting for server DRAM today. Management did not dispute the framework, only emphasized that even at that floor the margin beats prior cycle peaks. The way I read it: if the floor is half of today’s spot, then today’s spot is double what Micron themselves are prepared to sign as a five year bottom. So even Micron does not seem to believe current spot prices will last, and they are fine locking customers into long contracts at half of spot as a floor to secure volume and revenue. Are we looking at badly inflated spot prices that are about to cool down?

The capex is shifting from tooling to concrete. More than half of the capex increase planned for fiscal 2027 is construction, shells and cleanrooms, rather than wafer equipment. The cash goes out well before any new bits come out, so the supply response that would actually ease the shortage sits years away. That is a large part of why management is comfortable calling tightness beyond 2027.

Micron is reopening 1-alpha DDR4 production in Virginia to serve auto, industrial, medical, aerospace and defense. A node is just how advanced the process is, and DDR4 on 1-alpha is an older, mature one, what the industry calls trailing edge. A technology leader normally pushes its fabs toward the newest nodes and retires the old ones, because new parts carry the best price and margin. So reviving an old node is moving backward, and the act itself is the signal: the shortage reaches far enough down the product range that even low margin legacy parts are worth the capacity. The customer list says the rest. Auto, industrial, medical, aerospace and defense buy the same parts for years and often need domestic supply, so a US fab serving them is steadier, more predictable revenue than the volatile spot market, even at a lower margin.

Capital return is gated to a date. Buybacks were zero this quarter. Micron plans to step up capital return after December 9, 2026, the second anniversary of its CHIPS agreements, then move toward returning 100 percent of excess cash over time. The date reads less like a free choice and more like the point at which a constraint tied to the government incentives lifts. Either way it hands you a concrete moment to mark rather than a vague commitment.

The caveat I owe the thesis

Everything above is Micron’s view of Micron’s supply. The structural shortage call only holds if Samsung and SK Hynix do not add capacity faster than Micron assumes, and their prints are where I would verify that rather than take one supplier’s word for the whole industry. I have not reconciled their latest supply guidance against this here, so until I do, read the tight beyond 2027 line as Micron’s framing of the industry and not a confirmed industry plan. It is the single assumption that, if wrong, unwinds the rest.

Disclosure: The Best Ideas 2026 basket is ten equal weighted positions: Nvidia, Broadcom, Cadence, Vertiv, Powell Industries, Eaton, Micron, Arista, Credo and Astera Labs. The basket was recently rebalanced, adding Micron and removing Hubbell. Family account positions are disclosed separately when relevant. This is my own research and personal opinion, not investment advice. Do your own work before acting on anything here.